Card Ecosystem

Card Ecosystem

So you want to launch or integrate a card programme, where do you start?

Whether virtual or physical, debit, prepaid or credit - a trusted supply chain and partner based relationship will enable you to role out a solution in a timely manner.

So you want to launch or integrate a card programme, where do you start?

Whether virtual or physical, debit, prepaid or credit - a trusted supply chain and partner based relationship will enable you to role out a solution in a timely manner.

There are rules and regulations and geographical restrictions that will impact how your product will be constructed. You need a supply chain that can support you with market entry and with your growth strategy, whilst being flexible enough to realise your full product vision.

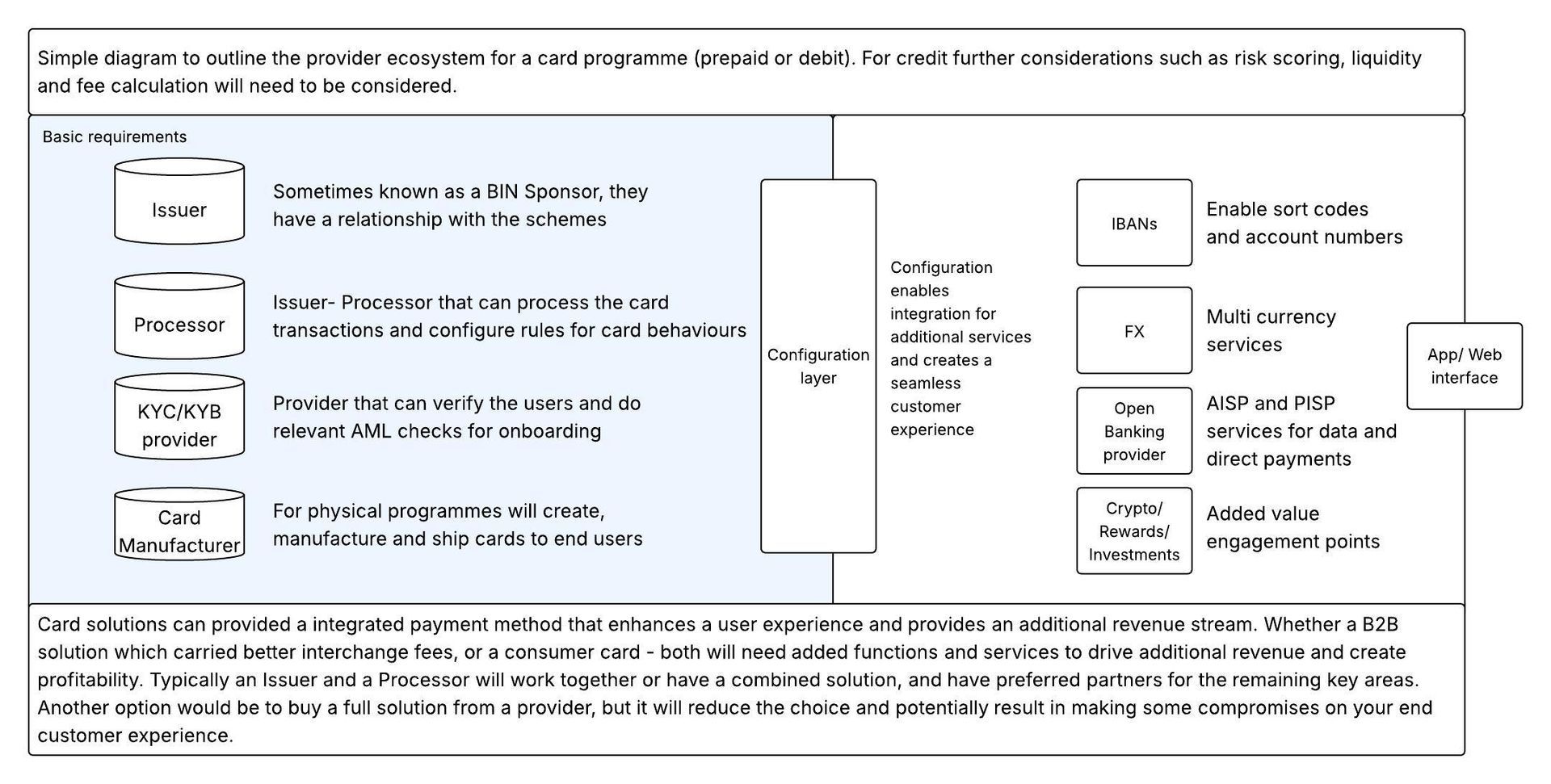

WHAT DO I NEED TO LAUNCH A CARD PRODUCT?

WHAT DO I NEED TO LAUNCH A CARD PRODUCT?

Before you launch any product that people can use to make payments, you need the right suppliers to help you bring that product to life. You can either negotiate and choose all parties in the supply chain and work with them directly, or you can work with a programme manager to provide fully managed services.

If you do choose to work with all parties directly you can be negotiating with seven plus entities, so be prepared to have a lawyer on standby.

Below we look at who you need in more detail:

SUPPLIERS BUILD FROM SCRATCH

You want to build from scratch and be the master of your own destiny? You will need certain companies to bring all the elements together. Below is a basic round up:

Scheme

The Scheme is the provider of the rails that your payment product will be riding. They enable your card payments to go through the system. Typically providers are Visa, Mastercard, Amex, China Union Pay, Discover and JCB but in some local markets there will be specialists.

You won't have a direct relationship with the scheme necessarily but it is worth being familiar with them as their logo will be on your card.

Issuer

The Issuer is the company that holds both an E-money Licence and has a licence with the Scheme. They are responsible for making sure your payment programme is compliant and adhering to scheme and government regulations. They provide you with the BIN (Bank Identification Number) that your programme will use. This is what identifies your programme to the rest of the payment ecosystem when used. You need all these elements to be able to initiate electronic payments. You do not need your own EMI licence, but you will need to work with an Issuer or BIN Sponsor that has one.

Issuer-Processor

The processor does just that, they process the payment transactions and hold the record of what funds have gone in and gone out. This is mainly on the card side of things, but some processors now offer agency banking (IBANs) which enables faster payments, SEPA, BAC's, CHAPS and Swift payments. You will need a processor to process the payments your customers want to make. You will also need them to monitor your transactions to ensure against fraud, put in relevant fee's and limits and generally configure your customer usage for the programme.

Card Bureau

Your bank does not make the plastic you use. A Card bureau manufactures, prints or embosses and programmes the chips on the card so that when you pop it into a terminal, the right information is exchanged to authorise the payment. The card bureau prints and makes the cards, they can also help with the card design to. All cards now have to be contactless which means customers can tap and make a payment when under a certain limit. Limit's vary by geographies.

Please note even with a virtual card programme you will still need approved artwork created that fits the scheme rules and will be shown to customers in digital form.

Other

You will also need a KYC or KYB provider to verify those that are applying for your product as who they say they are. You will need an open banking solution provider to allow for PSD2 if the product is to be used for day to day payments. You will also need a gateway if your product is going to be loaded from another card. You will need agency banking or open banking if it is going to be loaded from another bank account. You will need a website and app that works across all devices and can be added to frequently to future proof your product and maintain customer engagement.

Finally, you will need a settlement bank so you can manage your money.

SUPPLIERS - ONE SIZE DOES ALL

Rather than work with all these suppliers you can opt to have one contract and one set of commercials and these are provided by a programme manager. A programme manager has wholesale agreements in place with all the above elements and can provide you with a bundled solution - saving you time and money. For those starting out it can be a quicker and easier way to bring a minimum viable product to market whilst gaining revenue, and for others it is the security that certain elements are taken care of for you. This will be the first choice on your journey.

Then all you need is a great marketing strategy and a strong reason for customers to want your product. Does your product simplify an existing chore or make life easier for the client? How are you going to develop habitual use which will lead to loyalty?

Resources

Resources

Useful Resources

Issuers

- please note some have processing capabilities and more

Processors

UK/EU programme manager

Global programme manager

Membership organisations